January 7, 2021 •Michael Easterly

With contributions by Natalie Patten

Today’s post kicks off a three-part series on discrimination in mortgage lending and the analytical techniques that Summit Consulting uses to detect it. We use Home Mortgage Disclosure Act (HMDA) data, internal data from banks, and underwriting documents to detect and estimate potential predatory-lending practices for our clients.

Summit has supported investigations for the U.S. Department of Housing and Urban Development (HUD) and the Consumer Financial Protection Bureau (CFPB) since 2012.

Our comprehensive fair-lending analyses include:

Redlining is the discriminatory practice of denying or restricting credit to applicants based on the racial composition of the neighborhood where they want to buy a home. In other words, lending institutions practicing redlining deny loans in neighborhoods with a high percentage of minorities, even when applicants are creditworthy. While it was once a formal policy of private-sector lenders and the federal government, Congress outlawed redlining as part of the Fair Housing Act of 1968. Nevertheless, it persists today, usually in more subtle forms.

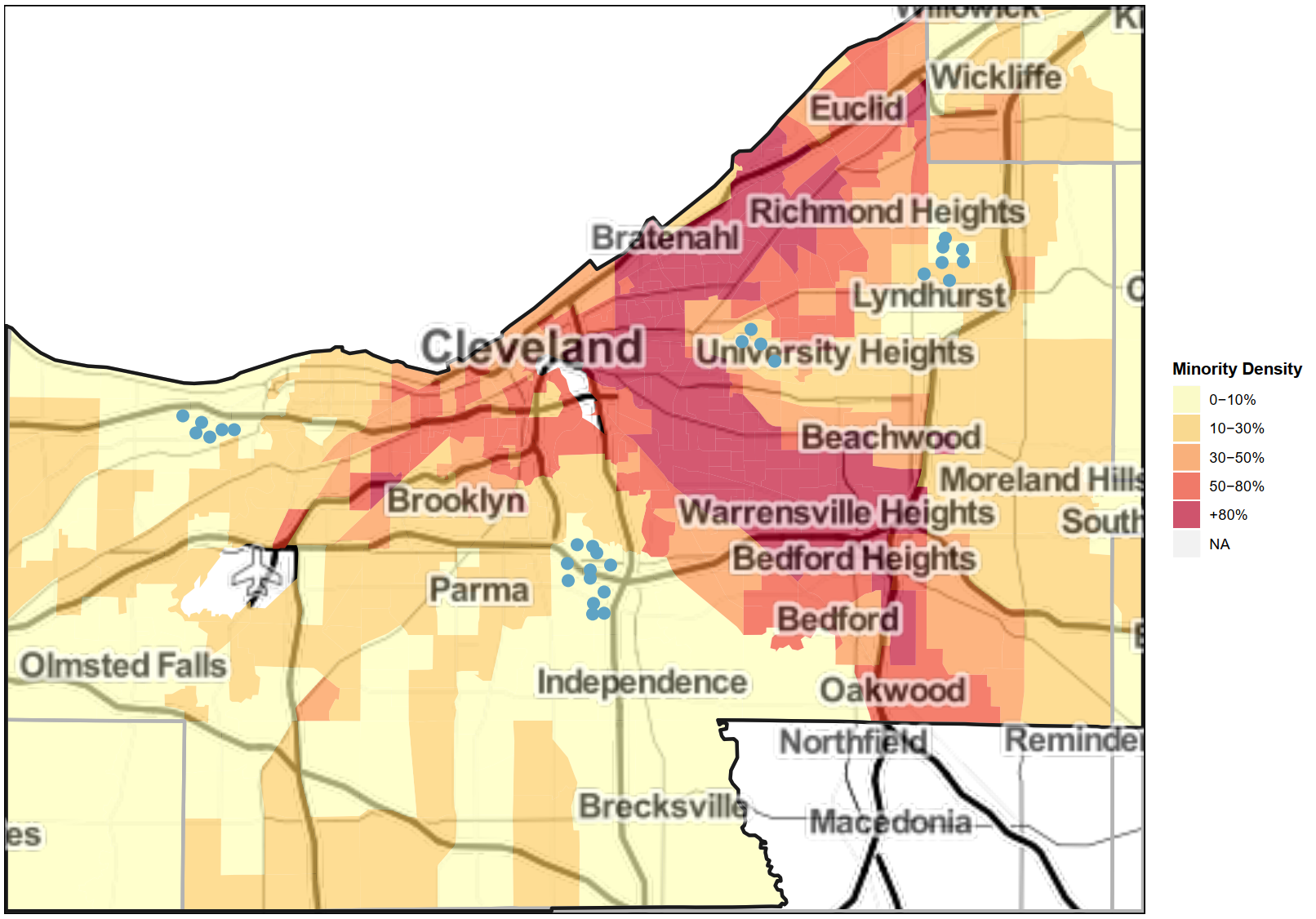

In the example map below, we show properties for which a hypothetical lending institution in the Cleveland metropolitan statistical area (MSA) approved loans. This lender appears to be engaging in redlining because most of the properties, shown as blue circles, are in neighborhoods with low minority populations (those with yellow or light orange shading). Although this map does not confirm that this lender is redlining minority neighborhoods, it does provide preliminary indications of redlining that should be explored further. We would then perform additional analyses to confirm the existence of redlining.

We conduct peer-institution comparisons to determine whether the lending institution we are investigating is unique in its alleged discriminatory behavior. If its peers have similar outcomes, this may indicate that there is a geographical pattern, such as a limited number of houses for sale in many high-minority neighborhoods, or other nonracial explanations for the origination patterns.

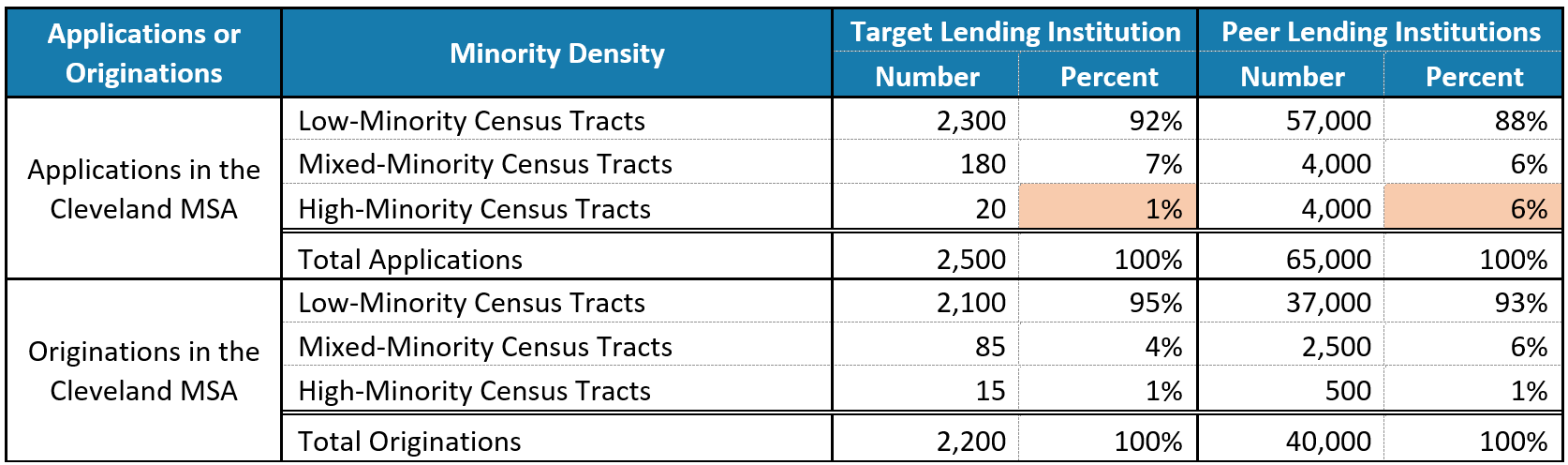

We identify peer lending institutions that are in the same geographic area and similar in size and lending capacity. First, we compare loan applications and originations in each minority density grouping (both low-minority and high-minority census tracts). Shortfalls in applications in high-minority areas relative to their peers may indicate that the lending institution’s marketing or business development teams are following discriminatory practices (for example, the lender does not market in high-minority neighborhoods). Shortfalls in originations in these neighborhoods compared to their peers may indicate that redlining is occurring in the approval process.

The table below shows that the hypothetical lender tends to receive fewer applications in high-minority census tracts than its peer lending institutions. This corresponds to a shortfall of 134 loan applications in high-minority census tracts. Therefore, we might conduct further analyses on nonracial neighborhood characteristics, such as income, that might explain why this institution does not lend in these areas. We might also encourage our client to investigate the lending institution’s marketing strategies.

In part two next Thursday, we’ll examine loan pricing discrimination, the practice of charging higher interest rates to minority applicants based on their race.