February 27, 2026 •Sarah Cunningham

By Sarah Cunningham, Crystal Wolf and Susan A. Betts. This article was originally published on January 8, 2026, in the AGA Journal of Government Financial Management, Winter 2026 Issue (Vol. 74, No. 4), pp. 58–60.

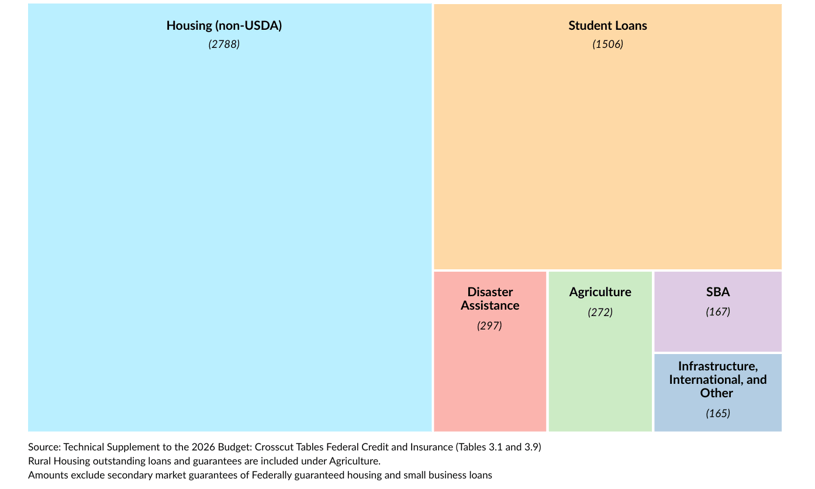

Federal loans and loan guarantees play a critical role in advancing federal missions. The U.S. government uses credit assistance to support national security, housing, small businesses, education, infrastructure, economic development, and more, as shown in Figure 1. With over $5 trillion outstanding, the U.S. federal credit portfolio is larger than the GDP of Germany, in and of itself the third largest GDP in the world.1 When one considers secondary market guarantees of federal small business and housing guarantees, the federal government manages over $8 trillion. The government serves tens of millions of borrowers—individuals, businesses, communities, nonprofits and sovereign nations. Over 42 million individuals have federal student loan debt.2 The Federal Housing Administration’s insured portfolio supported over 8 million single family mortgages last year.3 The U.S. Department of Agriculture’s Rural Development has over $263 billion in investments, with 60% in single family housing.4 Collectively, federal credit supports every aspect of our lives, directly or indirectly.

Figure 1. Federal Credit Loan Portfolio, Outstanding 2024 (in Billions of Dollars)

While these numbers illustrate the sheer scale of impact, capacity issues mean that there’s a lot that we don’t know about the credit portfolio. However, borrowers and the public expect a private-sector level of efficiency, transparency, accountability and positive customer experience. The Federal Credit Reform Act (FCRA) has made significant contributions to increase transparency, but the demand for credit programs has grown tremendously since FCRA was enacted in 1990. Unfortunately, the federal government’s capacity to implement federal credit programs hasn’t kept pace with the improvements in cost estimates nor has it realized benefits from private-sector advances in practices and technology. Legacy systems, manual processes and a lack of business requirements and system standards mean federal credit agencies must often recreate the wheel to establish systems and processes. There’s a chronic shortage of people that understand federal credit, and a lack of standard terminology and common understanding makes it ever harder for agencies to share knowledge and leverage shared systems or services.

These gaps create significant challenges for financial management. The 2024 Financial Report of the United States Government cited both Small Business Administration and U.S. Department of Education credit program weaknesses in internal controls that limited the reliability of financial data and increased errors that risk material balance sheet misstatements.5 Such findings have broader policy implications for the government’s ability to effectively allocate resources and will only reduce public trust.

Agencies need accurate and timely data to inform cost estimates and understand the financial performance of a credit program. Together with administrative and program data, agencies can tell the story of credit program performance (including cost-benefit analysis to understand the policy returns and impact of a program investment). Current gaps mean agencies lack complete data which contributes to an $8 trillion management problem. Manual processes and controls increase staff burden and reduce an agency’s ability to respond proactively to changing risk. It can also negatively impact the customer experience and the program’s impact. For example, manual reviews to approve disbursements can take significant amounts of time. For a borrower that needs the funds to close on a loan, that can mean costly delays. For a community building a safer intersection, induced project delays can lead to reduced public safety. When credit assistance is in response to economic crisis or disaster, timeliness is vital to recovery and stability. If an agency isn’t tracking key data points (or lacks expert analytic capabilities), it reduces confidence in cost estimates and may result in greater risk due to poor performance or risk indicators. Without timely and actionable analytics, the agency is blind—unable to spot trends and act quickly. Preventable losses are then only recognized after they occur. By modernizing the business of federal credit—through federal credit community engagement to develop standards, knowledge sharing, improved technology and a strengthened workforce—we can enable the federal government to better understand credit program performance, leading to improved impact.

Credit program management is complex, and effective implementation requires cross-disciplinary expertise and integration. Modernization is not easy, and modernizing a complex sector is even more challenging. Federal loans and loan guarantees are contracts that require non-federal borrowers to repay the loan with terms that can extend decades. To better account for the lifetime costs of loans and guarantees, FCRA requires these programs be accounted for on a present value basis—so policy officials and the public have a better understanding of the lifetime cost to government to inform decision-making.6 For example, FCRA budgeting enables the costs and benefits loans to be compared to grants or other forms of assistance. The investment impacts of a $10 million loan with an estimated budgetary cost of $1 million can be compared to a grant of $1 million. FCRA requires re-estimation of these costs each year, creating a feedback loop on how loans are performing relative to the initial cost estimate that provides better cost estimates over time.

While the budgetary accounting framework provided by FCRA enables better modeling and cost estimates, realizing the benefits of FCRA and federal loan and loan guarantee programs requires cross-disciplinary credit expertise. Federal credit has a specific financial management cycle, with strategic planning, budget formulation, budget execution, financial reporting and audit results feeding into the next cycle’s planning. It also has a credit program life cycle for the loan or loan guarantee that includes application, award, servicing direct or through lenders (disbursement, repayment, troubled loan servicing, remediation, recoveries), and closeout. Implementing guidance from the Office of Management and Budget (OMB) in Circular A-129, Policies for Federal Credit Programs and Non-Tax Receivables, lays out these responsibilities for OMB, the U.S. Department of the Treasury and credit agencies.7 Meeting these goals means agencies need federal credit subject matter expertise integrated across the board, including program, budget, performance, accounting and financial reporting, technology, project management and legal teams. Processes and systems should be designed or updated with an up-front understanding of what’s needed to fully realize the promise of FCRA. In addition to capturing necessary financial and non-financial data for cost estimates, performance and compliance, FCRA-specific technology standards and applications can enable automation of rote tasks, enable unified systems and approaches across programs, and free staff resources for analytics to drive continuous improvement, transparency and accountability.

Now is the time to solve the $8 trillion management problem. As the U.S. celebrates 250 years in operation, it is faced with more challenges at greater scale than ever before. Federal credit can be a powerful tool to achieve a variety of new and more challenging missions—and as the government shifts to a smaller footprint, leveraging technology to improve effectiveness, now is the time to utilize it accordingly. Given the complexity of the credit portfolio and each program’s current state, an agile approach to transformation (rooted in government-wide standards and requirements and workforce development) will build a stronger common basis for understanding, enabling incremental progress and allowing agencies to drive continuous improvement from where they are based on the specific needs of their programs. Fortunately, there are actions we can take to improve federal credit program management government wide.

Streamline federal credit requirements. OMB, Treasury, and the Federal Accounting Standards Advisory Board all have federal credit requirements for budget, performance, accounting, financial reporting and audit. Review implementing guidance, reporting requirements and standards to identify where there may be inconsistencies, duplications or opportunities to simplify. This would enable clearer business requirements and system solutions and is a start to a common lexicon that crosses disciplines and can inform congressional reporting requirements.

Establish standard business and system requirements for credit systems. Each credit agency (and in some cases each credit program) has built or added legacy systems to meet complex reporting requirements. Standard, objective-based requirements for credit systems can enable commercial off-the-shelf solutions (including software as a service solutions) for better origination, servicing and portfolio management that feed directly into financial and performance reporting. It can also offer opportunities for greater shared services or systems.

Develop workforce modernization resources. Establishing career roadmaps, skills and capabilities requirements, and resources for federal credit expertise (including general and discipline-specific training) would help de-mystify federal credit and help build an engaged, interdisciplinary approach to designing, implementing and improving federal credit programs. It could also build greater engagement across the federal credit community.

Engage the private sector and encourage public-private partnerships to drive innovation. The private sector has significant experience working with innovative technology and processes. The government could move faster by engaging the private sector and developing public-private partnerships through organizations like AGA to build capacity through collaboration on establishing standards, workforce development and resources along the way.

With $8 trillion in federal loans, loan guarantees and secondary market guarantees outstanding, tens of millions of borrowers, and the government’s reliance on federal credit as a tool to achieve its missions, the stakes are high for federal credit capacity. So are the rewards of modernization.

See: Joint Economic Committee, “GDP Update,” U.S. Congress, Sept. 25, 2025; and Jimenea, Adrian, John Wu, Harry Terris, Yuvraj Singh and Cheska Lozano, “The World’s Largest Banks by Assets, 2025,” April 15, 2025.

Federal Student Aid, “Federal Student Loan Portfolio,” U.S. Department of Education, accessed Dec. 1, 2025.

FHA, “Annual Report Congress Regarding the Financial Status of the Federal Housing Administration Mutual Mortgage Insurance Fund — Fiscal Year 2024,” U.S. Department of Housing and Urban Development, Nov. 15, 2024.

Rural Development, “Rural Investments in Program Areas,” U.S. Department of Agriculture, Dec. 7, 2025.

Treasury, “Financial Report of the United States Government — Fiscal Year 2024,” Jan. 16, 2025.

Under FCRA, costs are the present value of the lifetime payments and collections over time, excluding administrative costs.

OMB, “Circular No. A-129, Policies for Federal Credit Programs and Non-Tax Receivables,” Sept. 2024.

Sarah Cunningham, CGFM, a partner at Summit Consulting, is the vice chair of AGA'S CPAG Performance Improvement Committee and a member of the Finance & Budget Committee. Prior to joining Summit, she served at OMB and as a federal and local government executive. She is a member of AGA's Washington, DC Chapter.

Crystal Wolf, CPA, CGFM, CGMS, CICA, is the founder and CEO of Akela, a women-owned CPA firm specializing in federal financial management, risk and compliance. With nearly two decades of experience, she has supported some of the government's largest loan and grant programs, helping to advance program integrity and operational excellence. An active member of AGA since 2008, Crystal currently serves as president of the Washington, DC Chapter.

Susan A. Betts, CGFM, CPA, served as deputy assistant secretary for finance and budget at the U.S. Department of Housing and Urban Development, where she oversaw the Federal Housing Administration's financial management, budget formulation and execution, and note sales. She currently works as an independent consultant. Ms. Betts holds a bachelor's degree in accounting from Lehigh University.