March 13, 2017 •Edward Seiler, Ph.D.

On November 15, 2016, the U.S. Department of Housing and Urban Development (HUD) published the Actuarial Review of the Federal Housing Administration Mutual Mortgage Insurance Fund HECM Loans for Fiscal Year 2016. This review, prepared by HUD's independent actuary, contained several major methodological changes from the previous (FY 2015) version of the review. Those changes resulted in the economic value of the HECM portion of the Mutual Mortgage Insurance Fund (MMIF) falling to negative $7.7 billion from positive $6.8 billion the year before.

In these blog posts, two of Summit’s housing experts—Dr. Edward Seiler and Andrew Netter—provide an overview of the HECM reverse mortgage program and its mechanics and summarize the drivers of the changes between the 2015 and 2016 HECM Actuarial Reviews.

In our last blog post, we provided an overview of HUD’s Federal Housing Administration (FHA) Home Equity Conversion Mortgage (HECM) program with a focus on the program’s origins and how it’s changed over the years. In this blog, we describe the mechanics of how HECM loans work.

To be eligible for a HECM reverse mortgage loan, the borrower must meet the following criteria:

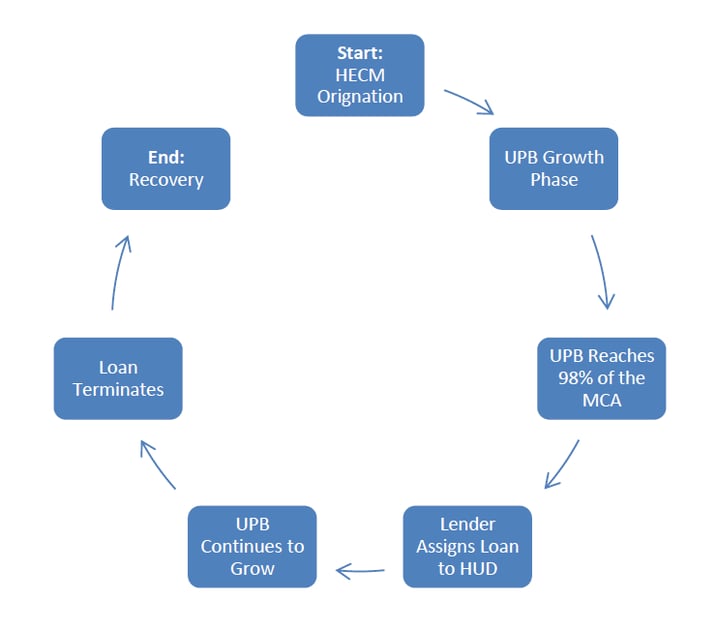

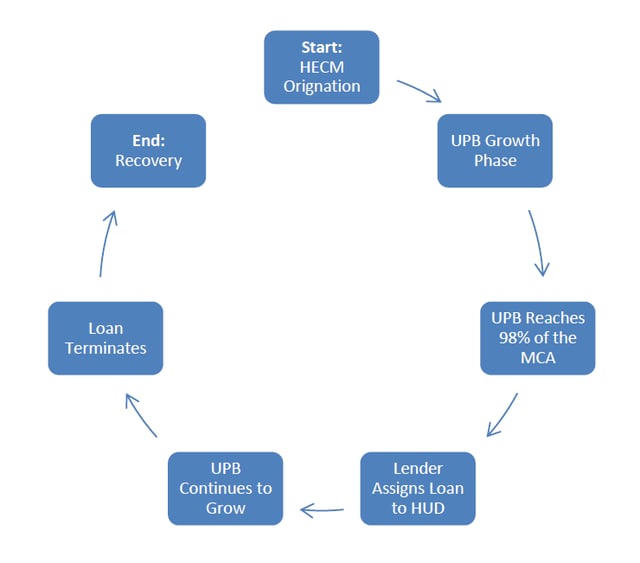

The maximum loan amount for a HECM is a function of two factors: the principal limit factors (PLF) and the maximum claim amount (MCA). The HECM originator establishes the PLF and MCA at loan origination, and they do not change over the life of the loan.

PLFs increase with borrower age at origination and decrease with interest rates at origination. The product of the PLF and the MCA is the initial principal limit. The amount the borrower is eligible to withdraw is the net principal limit, which accounts for loan proceeds used to satisfy other debts and obligations, including existing liens, closing costs, and set asides.

A HECM terminates when one of the following occurs:

In the latter two cases, we may call the termination a mobility termination or, if the borrower moves into a dependent care facility, a morbidity termination. Moreover, a HECM can terminate when the borrower defaults under the terms of the mortgage. Borrowers can default for several reasons, including not maintaining homeowner’s insurance, not performing required maintenance, and not paying property taxes.

A lender may file a claim to FHA for losses up to the MCA of each HECM. There are two such claim types:

At assignment, HUD purchases the loan from the lender for the minimum of the loan’s UPB and the MCA, and becomes the note-holder and servicer of the loan. The loan continues to accrue interest and MIP until loan termination. FHA pays all fees, cash draws, and other cash outflows monthly. Upon termination of the loan, the UPB is due and payable. This obligation can be satisfied by selling the home and remitting the net sales proceeds to HUD, even if less than the UPB, or by conveying the home to HUD. The borrower’s estate can also “purchase” the home for 95% of the appraised value.

We can summarize the lifecycle of a HECM that survives through assignment as follows:

Now that we’re armed with information about what the HECM is, in the next blog post, we’ll discuss some of the factors that drove changes in the HECM portfolio valuation between FY15 and FY16.